MAP in India: Resolving Cross-Border Tax Disputes Through the Mutual Agreement Procedure (MAP) | A Practical Guide for Multinational Businesses

As global commerce continues to expand, multinational enterprises increasingly face complex international tax disputes involving transfer pricing adjustments, permanent establishment allegations, withholding tax controversies, and instances of double taxation. In India, tax authorities have significantly intensified scrutiny of cross-border transactions, particularly involving related-party arrangements, digital economy structures, and global supply chains.

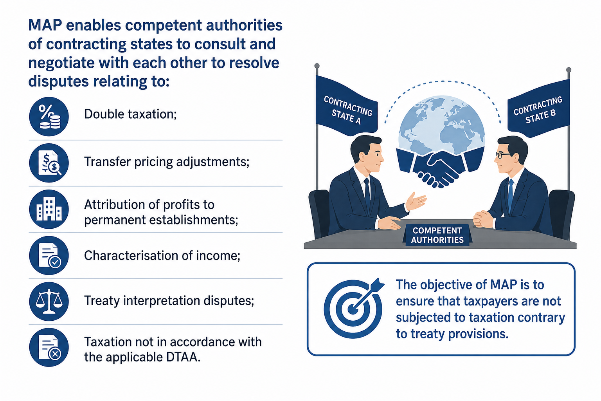

One of the most effective mechanisms available to taxpayers for resolving such disputes is the Mutual Agreement Procedure (“MAP”), provided under Double Taxation Avoidance Agreements (“DTAAs”) entered into by India with various jurisdictions.

MAP has evolved into a critical dispute resolution tool for multinational corporations operating in India, especially where unilateral tax assessments by two jurisdictions result in actual or potential double taxation.

This article examines the legal framework governing MAP in India, procedural aspects, recent developments, strategic considerations for taxpayers, and practical insights into handling cross-border tax controversies.

Understanding MAP Under International Tax Treaties

The Mutual Agreement Procedure is a treaty-based dispute resolution mechanism incorporated under Article 25 of the OECD Model Tax Convention and corresponding provisions in India’s tax treaties.

In India, the Competent Authority function is administered by the Foreign Tax & Tax Research Division (“FT&TR”) under the Central Board of Direct Taxes (“CBDT”).

Legal Framework Governing MAP in India

The statutory and treaty framework governing MAP in India includes the following key components.

Income-tax Act, 1961

Key provisions include:

- Section 90 and Section 90A of the Income-tax Act

- Rule 44G of the Income-tax Rules, 1962

- CBDT MAP guidance and circulars

OECD BEPS Framework

India is an active participant in the OECD Base Erosion and Profit Shifting (“BEPS”) initiative and has committed to implementing Action 14 relating to dispute resolution mechanisms and MAP effectiveness.

Situations Where MAP Becomes Relevant

MAP is commonly invoked in the following scenarios:

- Transfer Pricing Adjustments: Where Indian tax authorities make upward adjustments to the income of an Indian entity, while the corresponding foreign jurisdiction does not provide a corresponding adjustment, resulting in double taxation.

- Permanent Establishment (PE) Disputes: Where India alleges that a foreign company has a PE in India and seeks to tax profits attributable to such PE.

- Withholding Tax Classification Issues: Disputes concerning whether payments constitute royalty, fees for technical services, business profits, or interest income.

- Residence and Dual Residency Issues: Cases involving dual residency determinations under treaty tie-breaker provisions.

- Attribution of Income: Allocation disputes concerning profits attributable to cross-border operations.

MAP Procedure in India

Step 1: Filing the MAP Application

A taxpayer may file a MAP application before the Indian Competent Authority where taxation is inconsistent with treaty provisions. Applications are generally required to be filed within the time limit prescribed under the applicable DTAA, typically within 3 years from the first notification of the action giving rise to taxation not in accordance with the treaty.

Applications are submitted in Form No. 34F under Rule 44G.

Step 2: Preliminary Examination

The Indian Competent Authority examines admissibility of the application, treaty eligibility, whether the dispute falls within MAP scope, and availability of supporting documentation.

Step 3: Bilateral Negotiations Between Competent Authorities

Once admitted, the competent authorities of India and the foreign jurisdiction engage in consultations and negotiations. The taxpayer does not directly participate in these negotiations but may be required to provide information or clarifications.

Step 4: Resolution and Implementation

If an agreement is reached, the resolution is communicated to the taxpayer and acceptance is sought. Consequential relief is then granted through assessment modifications.

If the taxpayer accepts the MAP resolution, domestic remedies on the same issues may need to be withdrawn, depending on the circumstances.

India’s Evolving MAP Landscape

India has witnessed a substantial increase in MAP applications over the last decade. The CBDT has also issued administrative guidance aimed at streamlining the process and improving timelines.

India has increasingly demonstrated willingness to resolve:

- Transfer pricing disputes

- PE controversies

- Digital taxation conflicts

- Secondary adjustment disputes

Recent years have seen improved cooperation with jurisdictions such as the United States, Japan, and the United Kingdom, particularly in transfer pricing matters involving multinational groups.

Interaction Between MAP and Domestic Remedies

One of the most critical strategic considerations for taxpayers is the interaction between MAP proceedings and domestic appellate remedies. Taxpayers in India often simultaneously pursue:

- Appeals before the Commissioner of Income Tax (Appeals)

- Proceedings before the Income Tax Appellate Tribunal (ITAT)

- MAP applications

- Advance Pricing Agreements (APA)

Indian law permits parallel invocation of MAP and domestic remedies in many situations, although implementation of MAP outcomes may require withdrawal of certain appeals. Strategic coordination is therefore essential.

MAP and Advance Pricing Agreements (APA)

India’s APA programme has significantly reduced future transfer pricing litigation. In many cases, taxpayers pursue MAP for past assessment years and APA for future years.

This combined strategy offers long-term certainty and reduces recurring disputes. Rollback APA provisions have further enhanced dispute resolution efficiency.

Challenges Faced by Taxpayers in MAP Proceedings

Despite improvements, taxpayers continue to face practical and procedural challenges:

- Extended Timelines: Certain MAP proceedings may continue for several years, particularly where complex transfer pricing issues are involved.

- Information Requests: Authorities frequently seek extensive documentation and economic analysis.

- Lack of Transparency: Since negotiations occur between competent authorities, taxpayers may have limited visibility into discussions.

- Partial Relief: MAP may not always eliminate double taxation entirely.

- Non-Availability of Arbitration: Unlike some OECD jurisdictions, many Indian treaties do not provide mandatory binding arbitration.

Strategic Considerations for Multinational Enterprises

Businesses operating cross-border structures involving India should consider the following:

- Early Risk Assessment: Potential treaty disputes should be identified at the transaction structuring stage.

- Robust Documentation: Comprehensive transfer pricing documentation and treaty position analysis are critical.

- Coordinated Global Strategy: Tax and legal teams across jurisdictions must align positions before invoking MAP.

Evaluating MAP vs Litigation

Businesses should carefully assess:

- Time implications

- Cash flow exposure

- Reputational concerns

- Certainty of resolution

- Precedential impact

Recent Trends in India’s Cross-Border Tax Enforcement

Indian tax authorities continue to focus on:

- Digital economy taxation

- Significant economic presence concepts

- Substance-over-form analysis

- Beneficial ownership scrutiny

- Cross-border royalty structures

- Intercompany financing arrangements

Simultaneously, India has shown increasing engagement with international dispute resolution frameworks to improve investor confidence and treaty administration.

The government’s efforts toward faster MAP disposal are aligned with India’s broader objective of enhancing ease of doing business and reducing prolonged international tax disputes.

Best Practices for Businesses Engaging in MAP Proceedings

Multinational corporations should adopt the following best practices:

- Conduct periodic international tax health checks

- Align transfer pricing policies globally

- Maintain contemporaneous documentation

- Review treaty eligibility carefully

- Engage experienced international tax counsel early

- Monitor MAP timelines and procedural requirements across jurisdictions

Conclusion

The Mutual Agreement Procedure has emerged as one of the most important mechanisms for resolving international tax disputes involving India. As cross-border tax scrutiny intensifies, MAP offers multinational enterprises a structured avenue to mitigate double taxation and achieve treaty-consistent outcomes.

However, successful MAP outcomes require strategic planning, strong technical documentation, coordinated global tax positions, and careful management of domestic litigation exposure.

Given the increasing complexity of international tax enforcement, businesses engaged in cross-border operations involving India should proactively evaluate MAP options wherever treaty disputes arise.

Last Updated on 13 May, 2026

By entering the email address you agree to our Privacy Policy.